Narrow health care networks aren't actually that common

Published Date: 10/12/2018

Source: axios.com

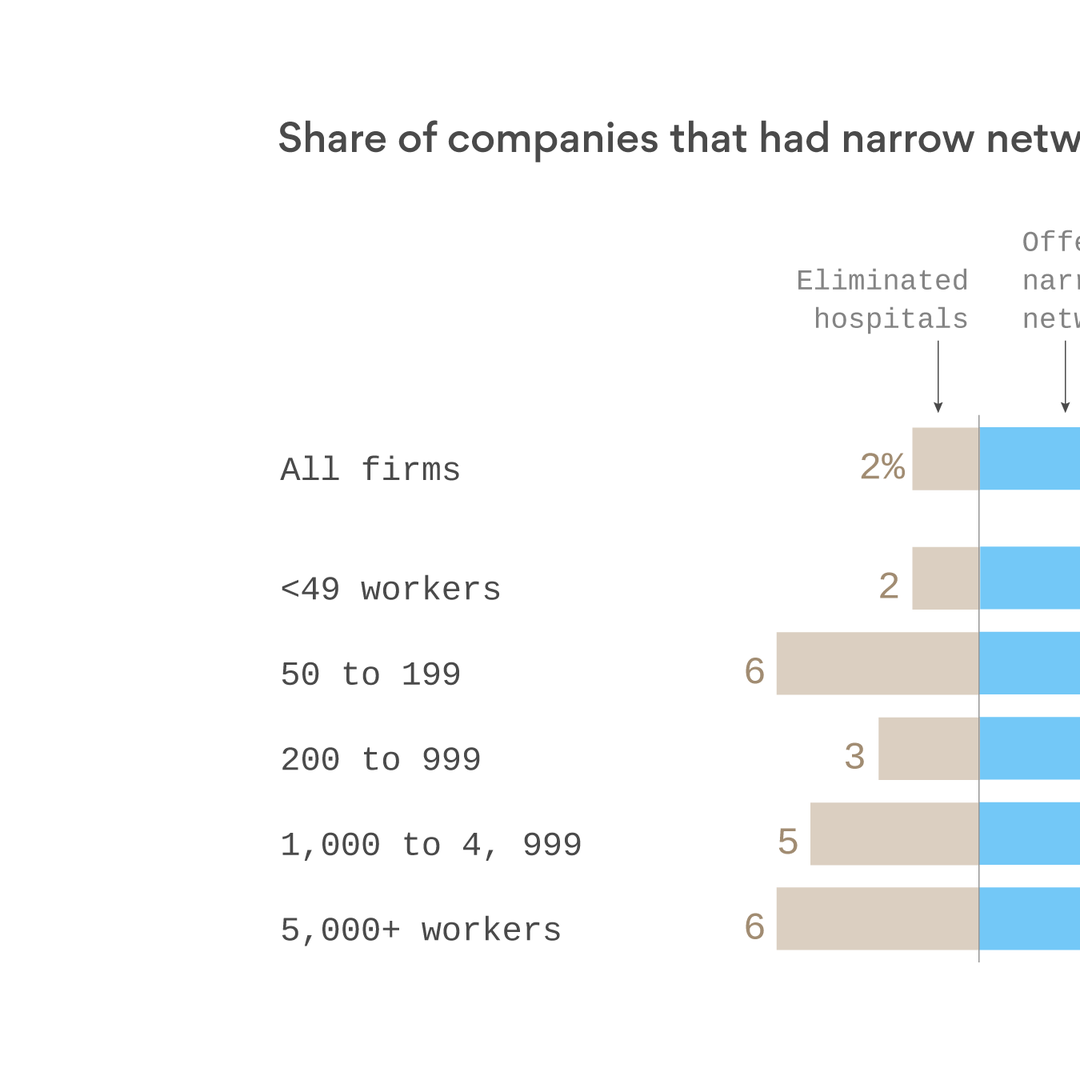

Adapted from Kaiser Family Foundation; Note: "There's been a lot of discussion of narrow provider networks and how they reduce costs by limiting access to the highest priced providers. They're commonplace in the Affordable Care Act marketplaces where about 10 million people are enrolled, and in the individual market generally but they are actually quite rare in the group market, where about 152 million Americans get coverage through their employers.Why it matters: Don't confuse the ACA with the health insurance market most people use. Narrow networks are the exception, not the rule, in the private insurance system overall, and there is little reason to believe that will change any time soon.The details: As the chart shows, only 7% of firms offering health benefits offer narrow network plans, and just 2% report that they or their insurer eliminated a hospital or health system from a provider network in the past year to reduce costs.By contrast, as Vitals has reported, narrow networks are much more common in the individual market. Just 29% of insurance plans in the individual market provide any benefits for out-of-network providers, down from 58% three years ago. In addition, a report by the consulting firm Avalere found that restrictive network plans made up 73% of the Affordable Care Act exchange market in 2018.Surveys also suggest that people who have been uninsured or buy their own coverage may be more willing to accept a tradeoff between provider choice and costs than workers in the group market.The big reason larger employers have not moved to narrow networks in significant numbers: its difficult for them to satisfy a diverse workforce with a limited network of doctors and hospitals, especially in a tight labor market. Its particularly difficult for them to exclude the most prominent (and often most expensive) providers.Where they are interested, they tend to promote what they regard as high performance networks that meet their guidelines for delivering high value care, not necessarily the lower cost networks more common in the non-group market.Between the lines: The public often has and is both intentionally and unintentionally given the impression that whats happening in the ACA marketplaces is happening the larger health system. Thats what happened when the general public believed that sharply rising premiums in the ACA marketplaces were affecting them when they were not.The debate over narrow networks has an impact on the ability of employers and insurers to control medical prices. While there are arguments for and against narrower networks, and the details matter, they are one of the few tools employers have to gain leverage over providers and put pressure on prices.If an employer (or insurers acting on behalf of employers) is not willing to exclude a particular hospital, it has no leverage in price negotiations. Mostly, employers and insurers are losing the price wars today.The bottom line: Controversial developments like narrow networks in the individual market deserve attention, but also context. They are still a rare bird in the group market where the largest share of Americans get their coverage.